Visualizing industrial job losses (Go Biz)

Can seasonality be traded profitably (CSS)

Short-trades are leading the upswing (WSJ)

Wednesday, September 30, 2009

Tuesday, September 29, 2009

IS-LM links of the day 9-29-09

August 7, 2008: Larry Summers on how to build a US recovery (FT)

A fair critique on why France is denouncing GDP as a measure of a country's wealth (WSJ)

A long term look at the VIX (VIX and more)

Which way does causality go with poverty and obesity (Slate)

In the newest installment of: and you call this news? The Times reports that 7 daughters of Goldman employees are sluts (NYT)

A fair critique on why France is denouncing GDP as a measure of a country's wealth (WSJ)

A long term look at the VIX (VIX and more)

Which way does causality go with poverty and obesity (Slate)

In the newest installment of: and you call this news? The Times reports that 7 daughters of Goldman employees are sluts (NYT)

Friday, September 25, 2009

Friedman Fact of the Day

How far away could you possibly be from a McDonald's (in the US)? Not more than 107 miles. (Source: Huffington Post)

IS-LM links of the day 9-25-09

Mark Thoma: What the unemployment numbers say (MoneyWatch)

Christina Romer says "Over? No, the recession isn't over" (WSJ)

Debit sucks as much as credit for the financially un-savvy (Cheap Talk)

An article on how financial services companies stick it to us with their innovative products and the case for a vanilla option (RortyBomb)

Can countries slash carbon emissions without harming growth? (Harvard)

A great idea re: gift bags coming out of the Clinton Global Initiative (NYT/Freakonomics)

Christina Romer says "Over? No, the recession isn't over" (WSJ)

Debit sucks as much as credit for the financially un-savvy (Cheap Talk)

An article on how financial services companies stick it to us with their innovative products and the case for a vanilla option (RortyBomb)

Can countries slash carbon emissions without harming growth? (Harvard)

A great idea re: gift bags coming out of the Clinton Global Initiative (NYT/Freakonomics)

Thursday, September 24, 2009

Likely Nobel Prize Candidates

Predictions courtesy of Thomson Reuters.

I like Weitzman or Taylor to pull through this year. I may even put my money where my mouth is and send in $2 to the contest that Mankiw is advertising.

Economic Heroes

David Klein of George Mason, a really hot department that people are talking about a lot these days, has a new article titled "In Defense of Dwelling in Great Minds." It's genesis is from his belief that reverence for particularly great economists has waned over time.

I think a spinoff of the argument is that, even if the majority of economists did have reverence towards deceased economists, they don't and probably can't feel the same way towards contemporaries. Dead economists, yes, people have the grace to honor the deeds and accomplishments of economists who came before them, but live contemporaries, no. I think this can best be supported from Klein himself: in his paper he offers a list of possible economic heroes:

One theme resonates through this list: the fact that all of those included are deceased. Additionally, I feel there is a serious omission from this list: he left out Paul A. Samuelson whose accomplishments would rate as one of the greatest of all time! I suggest that Klein overlooked Samuelson specifically because he is still alive. I don't consider this a major failing, just an interesting observation that could have been overlooked in his analysis.

If I were more cynical, I would argue that economists' pride in their own talent and intelligence precludes them from remonstrating to the mind of another. Those economists would decry their untimely date of birth which precluded them from publishing the same insights that won others acclaim. It goes without saying that this type of reasoning would have to work on a subconscious, or at the very least unspoken, level.

JDW

I think a spinoff of the argument is that, even if the majority of economists did have reverence towards deceased economists, they don't and probably can't feel the same way towards contemporaries. Dead economists, yes, people have the grace to honor the deeds and accomplishments of economists who came before them, but live contemporaries, no. I think this can best be supported from Klein himself: in his paper he offers a list of possible economic heroes:

such as Smith, Mill, Marx, Marshall, Veblen, Keynes,

Mises, Hayek, Rothbard, Galbraith, and Friedman.

One theme resonates through this list: the fact that all of those included are deceased. Additionally, I feel there is a serious omission from this list: he left out Paul A. Samuelson whose accomplishments would rate as one of the greatest of all time! I suggest that Klein overlooked Samuelson specifically because he is still alive. I don't consider this a major failing, just an interesting observation that could have been overlooked in his analysis.

If I were more cynical, I would argue that economists' pride in their own talent and intelligence precludes them from remonstrating to the mind of another. Those economists would decry their untimely date of birth which precluded them from publishing the same insights that won others acclaim. It goes without saying that this type of reasoning would have to work on a subconscious, or at the very least unspoken, level.

JDW

IS-LM links of the day 9-24-09

Fun Q&A session with Tim Hartford of the FT (NYT)

Fun Q&A session with Tim Hartford of the FT (NYT)The Soviets have a doomsday device and its still active (Wired)

Matthew Lynn declares winners and losers of the recession (Bloomberg)

Another opine on bank pay and the crisis (WSJ)

How Richard Posner became a Keynesian (New Republic)

Paul Farrell plots an anti-Michael Moore film espousing Reaganomics (MarketWatch)

CS Lewis's interesting observations (Chicago Boyz)

Wednesday, September 23, 2009

Hayek Original Haiku of the Day

Another day, another meeting. You don't have to know the topic of the meeting to understand the tempo.

Listening to this

blunts my senses like a fog

where did I flee to?

And a calculus one that has probably been invented before but felt good to create something intelligent:

The quotient rule: high

d low minus low d high

over low times low.

JDW

Listening to this

blunts my senses like a fog

where did I flee to?

And a calculus one that has probably been invented before but felt good to create something intelligent:

The quotient rule: high

d low minus low d high

over low times low.

JDW

Tuesday, September 22, 2009

IS-LM links of the day 9-22-09

It is finally here! Its another Nobel prize award season! Its like the Oscars for econonerds. Greg Mankiw has a contest and a list of possibles that are heavy publicants (GMB)

It is finally here! Its another Nobel prize award season! Its like the Oscars for econonerds. Greg Mankiw has a contest and a list of possibles that are heavy publicants (GMB)Ford's Free Trade story of the day (WSJ)

Monday, September 21, 2009

IS-LM links of the day 9-21-09

A great article on last words from death row inmates (NYT)

Greg Mankiw on Healthcare (NYT)

Tyler Cowen questions whether bank pay contributed to the crisis (MR)

The evolution of divorce: Class-based divorce (National Affairs)

Krugman vs Cochrane (Modeled Behavior)

A hilarious post on BofA's response to a House inquiry (Dealbreaker)

GM still has a massive quandery to ponder (Felix Salmon)

Greg Mankiw on Healthcare (NYT)

Tyler Cowen questions whether bank pay contributed to the crisis (MR)

The evolution of divorce: Class-based divorce (National Affairs)

Krugman vs Cochrane (Modeled Behavior)

A hilarious post on BofA's response to a House inquiry (Dealbreaker)

GM still has a massive quandery to ponder (Felix Salmon)

Sunday, September 20, 2009

Friday's inspired poetry

I attended meetings all afternoon on Friday. I learned a lot but my mind wandered as well, which produced these wonderful haikus:

This one was inspired by my econ professors:

data sweet data

SAS will strip, clean, and crunch you

so I can publish.

I want the money

I will do most anything

to fill up my account.

When you have no clue

just start talking until your

questioner gives up.

When you're in meetings

to sound important, speak in

abbreviations.

JDW

This one was inspired by my econ professors:

data sweet data

SAS will strip, clean, and crunch you

so I can publish.

I want the money

I will do most anything

to fill up my account.

When you have no clue

just start talking until your

questioner gives up.

When you're in meetings

to sound important, speak in

abbreviations.

JDW

Friday, September 18, 2009

Thursday, September 17, 2009

Obama on Healthcare

One of my favorite economists, Arnold Kling, writes a piece on the misstatements about Obama's healthcare plan.

I particularly like the characterization that Obama is trying to avoid the mistakes that Hillary Clinton made.

The conventional wisdom is that Hillary Clinton failed because she presented a plan and it was shot down. So it is really clever to not have a plan, and instead to get behind something that will pass and call it a plan. (Speaking of Hillarycare, its main source of funding was going to be cuts in Medicare and Medicaid reimbursements that everybody knew would never be adopted in practice. Apparently, Baucuscare retains that feature. The NY Times rounds up more commentary on the Baucus plan, which itself is not fully spelled out, although it runs to 225 pages.) If our democracy penalizes those who spell out their plans and rewards those who do not, then that is one more bad mark against our democracy.

I concur with Kling that it is very tricksy that Obama should continue to invoke "his" plan where none exists. But I wouldn't go so far as to say that it is "lying". (An aside: if Kling were a member of Congress he wouldn't be allowed to disseminate such utterances, reference). I would rather characterize it as quite deliberate politicking that he should allow the members of Congress to write, debate, revise, and pass a healthcare bill with only the most broad and general outlines of a plan that he could call his own (only bullet points really). While the media lambasts "Baucuscare", Obama will be left in the clear to mull with his mediocre approval ratings.

While I strongly believe that this approach is very smart and calculated, I don't think that this "hands-off" approach to governance is wise in the long-run. In the short term: it is unlikely that with a Democratic majority in Congress they will pass a plan that he radically disagrees with, but he is gambling with not having a big enough impact on an issue that obviously means a great deal to him. For instance, the public option is the point that most leftists want to see, and by-and-large seems to be fading in importance in all of the bills under consideration (to garner moderate support). In the long run, the risk Obama is playing with is not creating enough of a legislative imprint to be of any historical interest save for his election in the first place.

JDW

Wednesday, September 16, 2009

IS-LM links of the day 9-16-09

What economists believe (AEA)

Great Economics Equations (Environmental Economics)

-This guy definitely needs a quantity theory of money equation; Friedman would be mortified that his license plate (MV=PY) missed the cut

Interactive Labor Graph (flare)

The three most popular books at Guantanamo (Comment Central)

Great Economics Equations (Environmental Economics)

-This guy definitely needs a quantity theory of money equation; Friedman would be mortified that his license plate (MV=PY) missed the cut

Interactive Labor Graph (flare)

The three most popular books at Guantanamo (Comment Central)

Tuesday, September 15, 2009

Washington Post is on its way out the door

I like what Brad Delong has to say about the Washington Post.

I was able to pick up a free copy on my way out the door of my apartment complex and read it on the train. After two weeks of reading it from cover to cover I stopped picking it up and paid a subscription to the Wall Street Journal instead. That's right. My demand for Washington Post newspapers at a price that is zero is also zero, not nonzero like a downward-sloping demand curve would normally suggest!

I had a college friend come stay at my apartment with me and my girlfriend during the "trial period" previously alluded to. After reading only a page or two she puts the paper down, folds it, and says to me, "are all the articles this liberal or is it just the Sunday paper?" I laughed and agreed with her sentiment. (We both graduated with BAs in Economics and went on to graduate studies in Econ, so we're probably center-right).

Now, the only thing WaPo is good for are manufacturer's coupons in the Sunday edition (the paper goes unread back to the community pile). Only because when I show them to my girlfriend, her face lights up like a light (she loves saving money as much as I do-I'm a notorious miser; I pick up change everywhere).

What do you get when you combine an entire staff of writers with sophomoric ability and left-wing policy stances? Reduced readership and declining advertising.

JDW

Rediscovered Classic

I just re-read Paul A. Samuelson's classic (to me) piece: "How I Became an Economist"

I have always believed that the people who are good at what they do either work hard or have an innate ability. And for people who are really good, and Paul Samuelson was the best, they not only work very hard but they also more than three standard deviations away from the mean in terms of ability. Not only that, but they like what they do.

And my favorite quote:

I know that I have never been wanted to be considered overpaid, even by my own standards. But the sentiment is so heartening and selfless that I feel moved by it.

From one point of view my studying economics was the result of accidental blind chance. Prior to graduating from high school I was born again at 8:00 a.m., January 2, 1932, when I first walked into the University of Chicago lecture hall. That day's lecture was on Malthus's theory that human populations would reproduce like rabbits until their density per acre of land reduced their wage to a bare subsistence level where an increased death rate came to equal the birth rate. So easy was it to understand all this simple differential equation stuff that I suspected (wrongly) that I was missing out on some mysterious complexity.

I have always believed that the people who are good at what they do either work hard or have an innate ability. And for people who are really good, and Paul Samuelson was the best, they not only work very hard but they also more than three standard deviations away from the mean in terms of ability. Not only that, but they like what they do.

And my favorite quote:

Always, I have been overpaid to do what has been pure fun.

I know that I have never been wanted to be considered overpaid, even by my own standards. But the sentiment is so heartening and selfless that I feel moved by it.

Thank you, Dr. Samuelson, for your work, your writing, and your inspiration.

JDW

IS-LM links of the day 9-15-09

Arnold Kling's paper on the roots of the crisis is out (EconLog)

Cochrane and Zingales on one year after Lehman (WSJ)

Protectionism likely to rise (WSJ)

Krugman on the backlash from his magazine article (NYT)

Wine tastes different based on expectations (Science Daily)

Profile of Mr. Bubble-Robert Shiller

BIS Economist dampens mood, warns of double dip recession (FT)

Cochrane and Zingales on one year after Lehman (WSJ)

Protectionism likely to rise (WSJ)

Krugman on the backlash from his magazine article (NYT)

Wine tastes different based on expectations (Science Daily)

Profile of Mr. Bubble-Robert Shiller

BIS Economist dampens mood, warns of double dip recession (FT)

Monday, September 14, 2009

Friday, September 11, 2009

John Cochrane goes academic ape-s*** on Paul Krugman

John Cochrane totally rips Krugman a new ass in this article.

John Cochrane totally rips Krugman a new ass in this article. My favorite part of the article is:

Most of the article is just a calumnious personal attack on an ever-growing enemies list, which now includes “new Keyenesians” such as Olivier Blanchard and Greg Mankiw. Rather than source professional writing, he plays gotcha with out-of-context second-hand quotes from media interviews. He makes stuff up, boldly putting words in people’s mouths that run contrary to their written opinions. Even this isn’t enough: he adds cartoons to try to make his “enemies” look silly, and puts them in false and embarrassing situations. He accuses us of adopting ideas for pay, selling out for “sabbaticals at the Hoover institution” and fat “Wall street paychecks.” It sounds a bit paranoid.

It’s annoying to the victims, but we’re big boys and girls. It’s a disservice to New York Times readers. They depend on Krugman to read real academic literature and digest it, and they get this attack instead. And it’s ineffective. Any astute reader knows that personal attacks and innuendo mean the author has run out of ideas.

That’s the biggest and saddest news of this piece: Paul Krugman has no interesting ideas whatsoever about what caused our current financial and economic problems, what policies might have prevented it, or what might help us in the future, and he has no contact with people who do. “Irrationality” and “spend like a drunken sailor” are pretty superficial compared to all the fascinating things economists are writing about it these days.

How sad. (emphasis mine)

It may be hard for Paulie to sit down for a couple of days after that academic spanking from the Chicago school. You didn't really expect all the freshwater guys to just sit buy and let you take cheap shots at them, did you?

IS-LM links of the day 9-11-09

In the name of balance, I present to you: "How did Krugman get it so wrong?" A response to Krugman's lengthy NYT magazine article last week (Money Illusion)

A back-to-back good post by Scott Sumner (Money Illusion)

It pays to be nice (Newsweek)

Pat Buchanan asks if America is falling apart (WND)

Blueprint for regulation (Taunter)

Consumer sentiment is UP (Bloomberg)

Theodore Moran: When is a takeover a security threat (Vox)

Oil Speculators (Economist)

Follow up to "Judging Downturns" piece yesterday (Mankiw's blog)

Throwing jellyfish is illegal and hilarious (St. Petersburg Times)

A back-to-back good post by Scott Sumner (Money Illusion)

It pays to be nice (Newsweek)

Pat Buchanan asks if America is falling apart (WND)

Blueprint for regulation (Taunter)

Consumer sentiment is UP (Bloomberg)

Theodore Moran: When is a takeover a security threat (Vox)

Oil Speculators (Economist)

Follow up to "Judging Downturns" piece yesterday (Mankiw's blog)

Throwing jellyfish is illegal and hilarious (St. Petersburg Times)

Thursday, September 10, 2009

Obama's talk on healthcare

"They argue that these private companies can't fairly compete with the government. And they'd be right if taxpayers were subsidizing this public insurance option. But they won't be. I have insisted that like any private insurance company, the public insurance option would have to be self-sufficient and rely on the premiums it collects." -President Obama

The same was said about Fannie Mae and Freddie Mac. They were government sponsored entities that were considered to be "off-budget" of the government. And, for some strange reason, they paid around 40bps less than similarly-held investment grade bonds. You can devise any nomenclature that you want, but the fact remained that the government paid for that difference with its implicit guarantee of the bonds. (Financial interpretation: the default risk declined so the premium was reduced).

The exact same thing will happen again if a public option were to go forward.

JDW

IS-LM links of the day 9-10-09

Greenspan concedes to walk the plank and turns his back on the free market, admitting complicity in deregulation and apologizing for his hand in the crisis. Don't lament you old bean! You are the man and don't you ever forget that. You saved millions of people billions of $$ in interest. Just forget all about the much larger equity that vanished. (The Guardian)

Truly horrible news about poverty out today (Felix Salmon)

Is it the worst recession since the Great Depression? Yes, but that's a misnomer (Greg Mankiw)

Wednesday, September 9, 2009

Fed releases the Beige Book

Summary: here

Reports from the 12 Federal Reserve Districts indicate that economic activity continued to stabilize in July and August.

Hooray! The worst is behind us. We can celebrate.

Not so fast:

Labor market conditions remained weak across all Districts.

The theme among the drab, bureaucratic jargon seems to be that things may be getting worse, but not nearly as fast as they were. In math terms, the first derivative is still negative but the second derivative has now switched from positive to negative.

Everything is flat: sales, real estate (residential and commercial), tourism, wages (soft though), and agriculture.

Which begs the question: if everything is so bad, what is driving the stock market?

IS-LM links of the day 9-9-09

My favorite economist, Arnold Kling, on regulation and the crisis (JAEI)

Ed Glaesar on what we've learned from the housing crisis (NYT)

Capitalism After the Crisis (National Affairs)

Collateralized Death Obligations: Trading in Life Insurance (Felix Salmon)

Greenspan: Market Crisis 'will happen again' (BBC)

Will the demand for assets fall as baby-boomers retire? (CBO)

Why do college kids fail to finish? (NYT)

Ed Glaesar on what we've learned from the housing crisis (NYT)

Capitalism After the Crisis (National Affairs)

Collateralized Death Obligations: Trading in Life Insurance (Felix Salmon)

Greenspan: Market Crisis 'will happen again' (BBC)

Will the demand for assets fall as baby-boomers retire? (CBO)

Why do college kids fail to finish? (NYT)

Tuesday, September 8, 2009

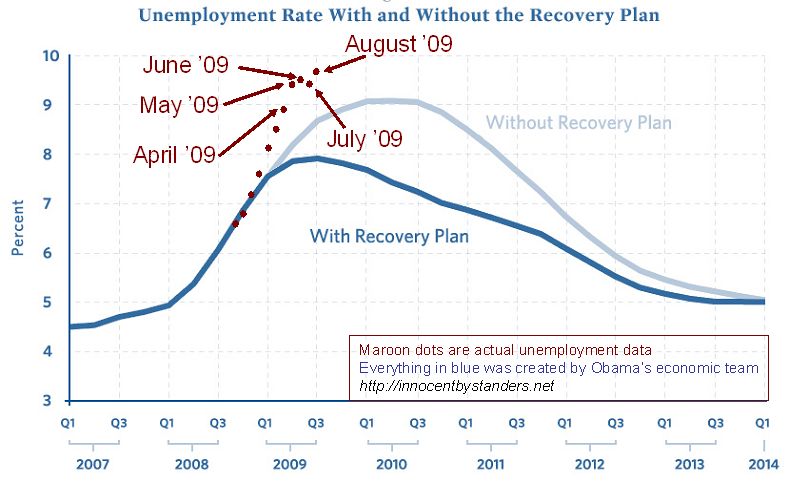

Unemployment Watch: 09-08-09

In May, the first time that I saw this graph, Greg Mankiw had an excellent post on his interpretation of these projections (link here). He proposed two reasons for the divergence: 1. the Stimulus has not enjoyed its desired effect or 2. the baseline projections used in the forecasts were too rosy.

I agree wholeheartedly with the latter, but the conclusion on the former is more of a mixed bag.

The grievance I have with the Stimulus is the timeline of the expenditure of the funds, which reminds me of a chi-distribution: proportionally less investment in the beginning (now, when we need it) with more following and eventually dissipating. To date, Recovery.gov reports that $88.8 of the $787 billion has been "paid out" (reference). Even with this likely inflated figure, it means that just 11% has been spent in the depths of the crisis. The consensus seems to be (from my reading and checked by the markets at http://www.intrade.com/) that GDP numbers will be positive in Q3 and Q4 of 09 on into Q1 of 2010. The Stimulus, then, will provide a boost to aggregate demand when it is less necessary; thus creating a lagged Keynesian fiscal expansion.

IF there is even a fiscal multiplier to speak of. A very big if. Volker Wieland (Vox) says there is none. This new working paper from the IMF which concludes that fiscally expansionary shocks are most effective when there is a (believable) commitment by the government to reduce expenditures in the medium term. And on the other side you have Christy Romer, whose paper came out in mid-January 2009, concluded the fiscal multiplier was approximately 3, and has since become a punching bag for stimulus detractors. (I even read it called a piece of "shlock economics").

My own opinion from the literature (which I buffed up on towards the end of grad school) is that the fiscal multiplier is between -0.5 and 1. That puts it in the realm of the opposite of its desired effect to effectively neutral. Stimulus, then, was perhaps not the best use of our national resources.

Time will provide the answer as to how much of a boost the bill provided, but I don't think it will be as positive as the Democrats who pushed it through would have you believe.

JDW

Friday, September 4, 2009

Have a great Labour Day Weekend

Ladies and Gentlemen:

I wish you the best over the holiday weekend. I plan to get out and enjoy it myself.

JDW

I wish you the best over the holiday weekend. I plan to get out and enjoy it myself.

JDW

Economics summarized in four panes

Thank you Greg Mankiw for point this comic from Prickly City out.

IS-LM links of the day 9-4-09

Un-Official List of Troubled Banks (Calculated Risk)

A lot of good recessionary data (Vox)

Unemployment hits 9.7%, higher than consensus (Bloomberg)

No demand, no inflation (The Money Game)

A House built from Legos (via MR)

Not quite the QB of the football team: Central Banks Popularity (Vox)

A thoughtful, Krugman piece of self-loathing on the state of economics (NYT)

A lot of good recessionary data (Vox)

Unemployment hits 9.7%, higher than consensus (Bloomberg)

No demand, no inflation (The Money Game)

A House built from Legos (via MR)

Not quite the QB of the football team: Central Banks Popularity (Vox)

A thoughtful, Krugman piece of self-loathing on the state of economics (NYT)

Thursday, September 3, 2009

<3 the guys at xkcd

IS-LM links of the day 9-3-09

Robert Fogel on why we are spending more on healthcare (JAEI)

The Stimulus seems to be helping (WSJ)

Behaviour economics of dating (Predictably Irrational)

The Economics of Fairy Tales (NYT)

To improve the value of my bachelor's, they should raise the tuition some more (NYT)

British Conservative Leader ringtones

The Stimulus seems to be helping (WSJ)

Behaviour economics of dating (Predictably Irrational)

The Economics of Fairy Tales (NYT)

To improve the value of my bachelor's, they should raise the tuition some more (NYT)

British Conservative Leader ringtones

Subscribe to:

Comments (Atom)

{kind=link}

{kind=link}

{kind=link}